Blue Origin’s rocket exploded on the launchpad in May. The single event moved AST SpaceMobile’s satellite-to-phone service back to early 2027. AST wants $1 billion — partly to buy its own launch capability, so this never happens again.

AST SpaceMobile’s commercial service delay was confirmed through an SEC filing — the company’s first official acknowledgment that its satellite-to-phone launch plan is running behind schedule. AST SpaceMobile expects approximately 45 satellites in orbit by early 2027, down from its previous target of launching that same fleet count during 2026 — a target CEO Abel Avellan reiterated as recently as the company’s first-quarter earnings call in May. Alongside the delay, AST SpaceMobile raised approximately $1 billion in convertible debt notes, with roughly $900 million earmarked to secure additional launch capacity — including potential partnerships or acquisitions to vertically integrate its own launch capability and reduce dependence on third-party providers.

What’s Happening & Why It Matters

The Blue Origin Domino Effect

AST SpaceMobile’s commercial service delay traces directly to a launch vehicle disruption TF has covered extensively across 2026. Blue Origin‘s New Glenn rocket experienced a ground test anomaly resulting in an upper-stage explosion during a late-May static fire test, sidelining the vehicle and limiting near-term launch availability across the entire industry. That setback follows a separate earlier loss — the atmospheric reentry and loss of BlueBird 7, which failed to reach its targeted orbit following an off-nominal upper-stage engine burn earlier in the year.

By contrast, AST SpaceMobile has continued launching satellites through alternative providers throughout the disruption. The company recently used SpaceX‘s Falcon 9 to launch BlueBirds 8, 9, and 10, with BlueBirds 11, 12, and 13 scheduled for an August launch. Investment bank William Blair, in a research note published in early June, estimated the Blue Origin setback alone would delay commercial services by three to six months — an estimate that has been confirmed as accurate by AST SpaceMobile‘s own regulatory disclosure.

The $1 Billion Bet: A Way Out of Dependency

AST SpaceMobile’s commercial service delay produced a specific strategic response beyond simply waiting for launch capacity to recover. The company indicated it intends to use the debt proceeds to pursue “growth initiatives” and to “secure additional access to orbit for its space-based cellular broadband network, including partnerships and/or acquisitions to vertically integrate its business and mitigate risks associated with third-party launch providers.” AST SpaceMobile clarified it does not currently have any “understandings or agreements” for such transactions — the funding is precautionary and forward-looking rather than tied to a specific pending deal.

That vertical integration ambition mirrors a strategic principle chief strategy officer Scott Wisniewski articulated publicly in May: “Our strategy has always been to have many launch providers… We have been developing other heavy launch providers for some time.” Following the SEC filing, ASTS shares fell 3.6% as investors weighed the new convertible note offering against dilution concerns, the delayed timeline, and continued questions about the company’s cash burn trajectory.

The Race Against SpaceX’s Direct-to-Device Plans

AST SpaceMobile’s commercial service delay carries a specific competitive cost that industry analysts flag directly. Every month AST SpaceMobile‘s commercial launch is delayed gives SpaceX additional runway to build partnerships with wireless carriers and lock in customers before AST SpaceMobile can offer a competing service. As TF covered in its SpaceX shares article, SpaceX already operates its own direct-to-device Starlink service with millions of subscribers, and just raised billions in its record June IPO to fund future expansion.

By contrast, SpaceX carries a structural advantage AST SpaceMobile cannot easily replicate — its own rockets. Competing with SpaceX is “not going to be easy,” analysts note, precisely because SpaceX controls its own launch vehicle supply chain end-to-end, while AST SpaceMobile is dependent on exactly the third-party providers — Blue Origin and SpaceX itself — whose disruptions just cost it a year of schedule.

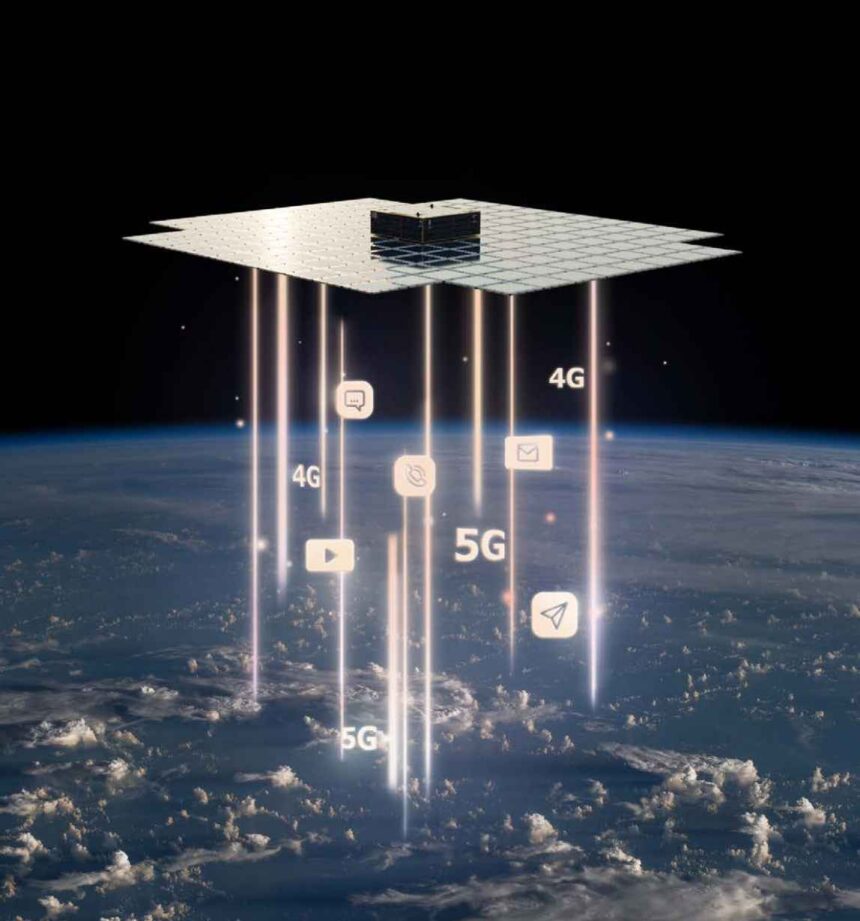

What 45 Satellites Gets AST SpaceMobile

AST SpaceMobile’s commercial service delay matters because of a specific technical threshold the company has not yet reached. Even if the BlueBirds scheduled for August launch successfully, the company still has a long path before reaching the 45 to 60 satellites needed for continuous coverage in key markets. AST SpaceMobile‘s original plan targeted deploying 45 to 60 satellites by 2026 to support continuous service in the US, Europe, Japan, and other strategic markets, including US government applications — with anchor carrier partnerships already signed with AT&T and Verizon in the US, and a 10-year commercial agreement with stc group covering Saudi Arabia and regional markets.

Valuation depends heavily on proving the company can move from technology demonstration to commercial service at scale — a transition the 2027 delay pushes back by roughly a year from the original fourth-quarter 2026 target investors had priced in.

TF Summary: What’s Next

BlueBirds 11, 12, and 13 launch in August 2026. 45 satellites are targeted for orbit by early 2027, versus the previous late-2026 goal. AST SpaceMobile continues evaluating launch vehicle partnerships or acquisitions with the newly raised $1 billion, though no specific transaction has been confirmed. The company’s anchor carrier agreements with AT&T, Verizon, and stc group are in place independent of the launch timeline shift.

MY FORECAST: AST SpaceMobile’s commercial service delay will not be the last schedule revision the company issues before reaching full commercial service — launch vehicle dependency is the single largest risk factor in its business model, and neither Blue Origin nor SpaceX can guarantee disruption-free manifests going forward. By contrast, the $1 billion raise specifically targeting launch vertical integration is the correct strategic response — a company whose valuation depends on satellite deployment cadence cannot hold permanently hostage to third-party launch schedules. Expect AST SpaceMobile to announce a specific launch capability partnership or acquisition within 12 months, given the scale of capital earmarked for exactly that purpose — and expect SpaceX‘s own Starlink direct-to-device expansion to capture meaningful additional carrier commitments during the window this delay creates.

Related Stories

- SpaceX Shares Fall Below Their IPO Price

- Space Racers: Impulse’s Big Raise, Blue Origin’s Timeline, and SpaceX Starfall

- NASA Commits $590 Million to Four New Lunar Missions