Alphabet unloads its Fiber side project to established teleco provider, Astound.

Google Fiber is heading into a merger with Astound Broadband after a sale to a private equity firm, according to the uploaded report. The merger would combine one of the most closely watched fiber brands in the U.S. with a cable-and-fiber operator that already grew through earlier consolidation. The result could create a broadband company passing about 7.1 million locations across 26 states.

Google Fiber has long lived in a strange space. It was too real to ignore, yet too limited to change the market fully. The deal could change that. It could turn a once-disruptive brand into part of the very consolidation story it once challenged. That irony has some bite.

What’s Happening & Why This Matters

The Deal Would Create a Much Larger Footprint

The uploaded report says GFiber serves 2.8 million locations in 15 states. Astound serves 4.45 million locations in 12 states and the District of Columbia. Astound’s network is mostly cable broadband. It includes 892,014 fiber locations and 44,548 copper locations. Together, the two companies would cover about 7.1 million locations across 26 states.

That size changes the conversation fast. Google Fiber has long carried a reputation that exceeds its physical reach. The brand compelled incumbents, scared cable operators, and made cities dream about fiber competition. Yet it still covered a modest slice of the country. Astound adds actual scale. It also adds density in markets where the combined company could matter more to pricing, upgrades, and local rivalry.

The report says the overlap is surprisingly small. GFiber and Astound overlap in only three Texas counties, covering about 109,000 locations. That low overlap helps the merger look more additive than duplicative. Texas and Illinois would hold the largest footprint for the combined company. Cable and fiber would each cover nearly equal shares of total locations.

That balance matters. It gives the combined company a wider menu of infrastructure options. It raises a harder question: will it keep pushing fiber, or will it get lazy and milk cable where it can?

Google Fiber May Gain Scale, but Risks Losing Its Edge

Google Fiber built its name by forcing the broadband industry to sweat. It showed up in city after city, promised faster fiber, and made incumbent providers move faster than they wanted. Even where Google Fiber did not launch, the threat often mattered.

A merger changes that identity. The uploaded report says Astound is already the product of earlier private equity deals that combined Wave Broadband, RCN, and Grande Communications. That means GFiber would no longer sit apart as a tech-company broadband experiment. It would sit inside a larger consolidation machine.

That may help operations. It may also dull the brand.

There is a clear upside. A larger entity can spread fixed costs, negotiate more effectively with vendors, and invest across a wider range. It can use Google Fiber’s name to stretch in fiber-rich markets while leaning on Astound’s scale in cable-heavy territory. If managed well, that could turn GFiber into a more credible national challenger.

There is a clear risk. Private equity deals don’t usually make people think of lower bills, friendlier service, and patient long-term network upgrades. They make people think of leverage, cost-cutting, and spreadsheets with a cruel little grin. Google Fiber’s old image as the cleaner, faster alternative could get tangled in that perception very quickly.

That is the brand problem at the center of this deal. Growth is useful. So is trust. Mergers often help the first and bruise the second.

Competition Will Still Exist, but the Questions Get More Interesting

The uploaded report says the combined GFiber/Astound company would still face at least one cable or fiber-or-copper competitor across most of its footprint. It lists AT&T at 53% of locations, Comcast at 46%, Charter at 43%, Verizon at 22%, and Lumen (CenturyLink) at 11%.

So this is not a story about one giant swallowing the field whole. It is a story about repositioning inside a crowded broadband map.

Still, those numbers do not settle the most important issue. Local broadband markets are not considered competitive simply because another provider exists on paper. They are competitive when customers can actually switch, get comparable speeds, and avoid being punished with pricing games, installation delays, or confusing bundles.

That is why the report’s “unanswered questions” matter more than the raw footprint math. The analysts ask whether the combined company will continue expanding into markets already served by existing cable and fiber operators. They ask whether it will expand Astound’s cable footprint with additional fibre.

Those are the real pressure points.

If the combined company keeps building fiber into areas that already have cable and legacy broadband, it could still act as a meaningful challenger. If it slows expansion and starts optimizing the existing map, then the deal may look less like competition and more like comfortable consolidation. Consumers know that script well. It usually ends with a press release about “enhanced capabilities” and a bill that somehow still climbs.

Geography: Momentum or Retreat

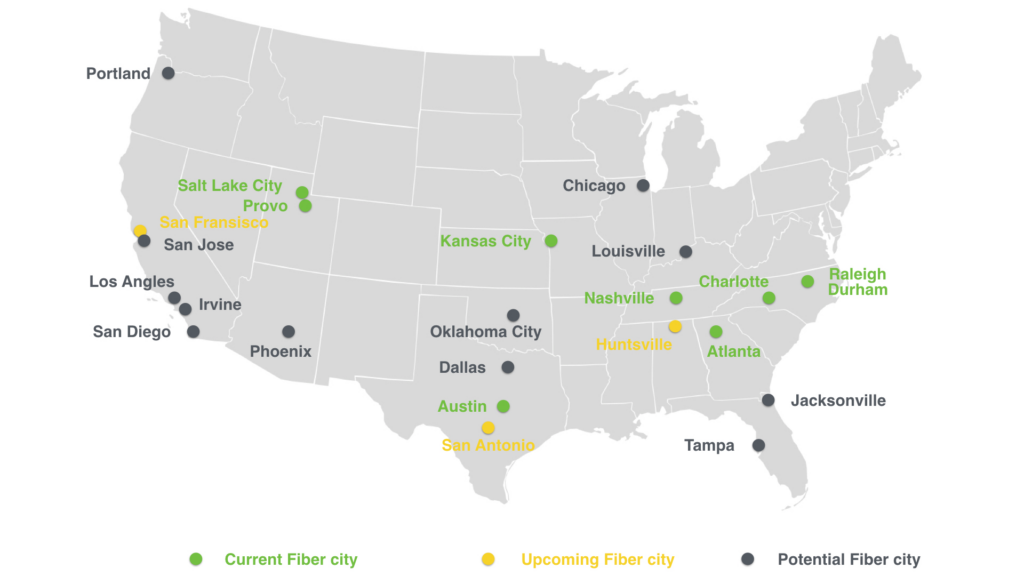

The file gives a clear view of where the combined business would matter most. Texas, North Carolina, Missouri, Utah, and Kansas account for about 78% of GFiber locations. For Astound, Illinois, Texas, New York, California, and Washington make up about 72% of locations.

That concentration matters because it creates strong regional clusters. It means the story is not the same everywhere.

In Texas, the merger could matter a lot. The overlap is limited, yet both companies already have a meaningful presence there. In Illinois, Astound’s footprint makes the combined company more visible. In states where Google Fiber has built strong local recognition, the merger may look like a scale play. In places where Astound dominates the customer relationship, Google Fiber’s role may feel more like a brand asset folded into a bigger operation.

That split creates a strategic choice. Does the merged company use the Google Fiber name as the growth spear? Or does it quietly absorb that reputation into a more conventional broadband structure?

The answer will show what the deal really means.

Google Fiber’s legacy is not only about network mileage. It is about expectation. People saw the name and expected faster fiber, cleaner pricing, and less nonsense. If the merged company preserves that expectation and expands on it, the deal could be a good one. If it waters down the brand inside a bigger cable-heavy machine, then Google Fiber may end up as one more example of a bold idea that the market eventually filed smooth.

TF Summary: What’s Next

The uploaded report points to a sale of Google Fiber to a private equity firm and a merger with Astound Broadband, creating a company that would cover approximately 8 million locations in 26 states. GFiber brings 2.8 million locations in 15 states. Astound brings 4.45 million in 12 states plus D.C. The overlap is small, with only three Texas counties and about 109,000 shared locations.

MY FORECAST: This deal will look smart on paper right away. The harder test will come later. If the merged company continues to advance fiber upgrades and aggressively infiltrates contested markets, it could still carry some of Google Fiber’s old disruptive spirit. If it slows, builds, and leans into cable economics, the merger will look like another consolidation move dressed in growth language. Broadband buyers do not care much about deal structure. They care about speed, price, and whether the service stops acting like a hostage note.

— Text-to-Speech (TTS) provided by gspeech | TechFyle